© 2019 -2020 BadlyTreated.All rights reserved

BadlyTreated

Reports

Our first report involves an Insurance Company widely advertised on Social Media and Comparison sites. The Company is called

Policy Expert

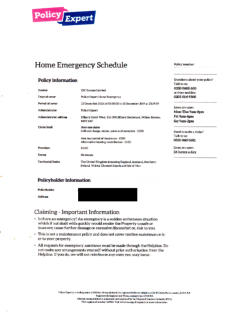

On 12th December 2018 a Home Insurance Policy Building and Contents Insurance was purchased from Policy Expert this also included Home

Emergency Cover.

On the 14th July 2019 it was found necessary to contact the Home Emergency help line. A leak was discovered coming out of the brickwork of the

property outside wall. The Policy home owner could not discover where the water was coming from and was concerned further damage would be

caused.

The agent from the Home Emergency said after an ‘interrogation’, the Home Emergency Policy did not cover outside issues, only internal damage

therefore it was not covered.

It was explained that the policy holder was disabled and did not have the expertise that a plumber would have to find the cause of the leak and

ascertain the internal damage.

The Policy Holder was told perhaps they may be able to claim on their Home Insurance Policy as this was not an emergency.

Due to the fact that the Policy Holder was concerned about the issue a reputable plumber was called.

After some time investigating the plumber found the cause of the leak and carried out repairs and took photographs of the external and internal

damage.

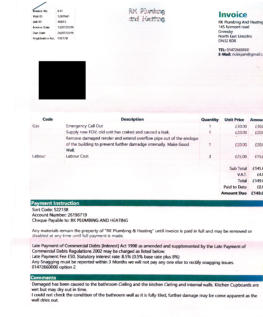

The plumbers report states: ‘Emergency Call Out. Supply new FOV, old unit cracked and caused a leak. Remove damaged render and extend overflow

pipe out of the envelope of the building to prevent further damage internally. Make Good Wall.’

Plumber Comments ‘ Damage has been caused to the bathroom Ceiling and the Kitchen Ceiling and internal walls. Kitchen Cupboards are wet but may

dry out in time. I could not check the condition of the bathroom wall as it is fully tiled, further damage may be come apparent as the wall dries out’

Personal details are blanked out for protection

of the householder/policy holder.

Clicking on the documents will take you to an

enlarged version.

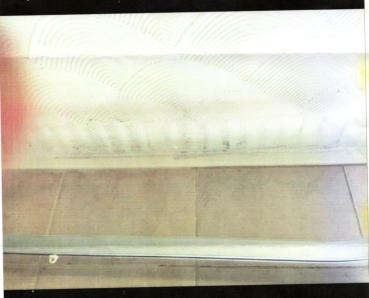

Photos of Damage

Bathroom Ceiling

Before Remedial Work

Issue Found

Photographs of the damage caused to the kitchen area could not be taken due to area not accessible

Cause Of Damage

This toilet is situated upstairs in the property and

was installed when the property was built (I

understand) in the 1950s.

The plumber said the FOV had cracked causing a

leak, the excess water drained okay through the

overflow on the left. However when the water

reached the overflow pipe to the property outside

wall it could not escape because the builders had

cemented over the pipe (in the 1950s) The plumber

rectified this by extending the overflow pipe and

then making good the render.

Policy Expert conclusion.

Policy Expert say they cannot payout on this claim because the issue was caused by ‘faulty workmanship’ however they advised to open the windows

and put the heating on so that the damage would dry out. (Faulty workmanship in 1950’s when the property was built)

How I can be at fault when the property was built in the 1950s and I purchased it in 1999 after having a full home purchase survey is beyond me.

In view of this I felt it was necessary to cancel the policy with Policy Expert straight away as if something major was to happen in the future they

would find some way of getting out of paying. A new policy was taken out with a reputable company. The matter is been reported to the

Ombudsman

UPDATE

To report a matter to the Financial Ombudsman, first a ‘Deadlock Letter’ has to be obtained. This was requested from Policy Expert on 6/08/2019 they have 14 days to reply. On 8/8/2019 Trinity Claims who act for Policy Expert informed me they will now be paying out on the claim and it should be in my bank within 14 days

LENSFLARE

© Lorem ipsum dolor sit Nulla in mollit

pariatur in, est ut dolor eu eiusmod lorem